Lovable

The case for Europe's first trillion-euro company

Startups are an outlier business. The most important companies create something altogether new in the world and grow extremely fast because they offer the world something previously unprecedented and useful. Building something that novel is risky. You’re doing something so new that it’s hard to know whether you succeed and what will happen, and there are many ways it could go wrong.

The best founders know a secret, a non-obvious truth about the world that others don’t know of yet. They have a vision of what the world looks like if they act on the secret and how that will change the world around us. Since change is hard and it’s easy to see so many ways the company can fail, investors also need to imagine how successful the company could be if the secret is true and things go really right in building a company around that secret, or it wouldn’t make sense to invest all that money into such risky projects — the investors need to be able to see the founder’s vision to have the confidence to put the money on the line. This does not mean the company gets there, but if it does, it’s important to understand the magnitude of the success to make the venture math work. In fact, this is why venture capital works: The companies venture capitalists invest in can be such massive outliers that it does not matter if some of the investment will fail as long as at least one works really well. This power law means that even if things go really right with one company of such explosive potential, the venture capitalist makes up for all of the other failed investments and ends up making money on top of that. These companies normally even surprise the founders, employees and investors how large they can get, and it’s exactly these companies that will end up changing the world for all of us.

There’s a lesson here. When we look at the startup founder building these high risk companies, we are quick to point out all the ways the companies might fail (and there are many) or how they are breaking many of the conventions we are used to. While being critical of the idiosyncratic nature of these founders and their companies, we should also ask what they could achieve if things go really right. It’s exactly when someone is taking the leap to create something new in the world, and when things go really right that the world will change and we all benefit from it. In fact, it’s only such ventures that take the world forward.

Lovable

Earlier I made the claim that the Nordics and Baltics are on their way to see the first Trillion-euro company in the next 10 years. To back up the bold claim, below I’ll make the case why Lovable has a shot if things go really right for them.

I want to make the argument especially now that there are screenshots circulating suggesting Anthropic might be releasing a similar app builder that Lovable is famous for. Sure, this is a threat, and the app layer is structurally disadvantaged, but this goes into what it means to be one of the fastest growing companies in history of the world — if you’re category leader in one of the largest and fastest growing markets in the world, you will invite serious competition at some point. That is the nature of building something very valuable. Let’s get to it.

A Trillion

In How to build a trillion-dollar company, I wrote: Trillion-dollar companies never look like one initially, but when the founder’s interest overlaps with the large technological currents impacting the core arteries of our future, giant companies are born.

The largest technological current today is the emergence of Artificial Intelligence, and the first killer app of the AI wave is AI writing software. For anyone being able to program by describing what they want in plain English is such a big unlock that it really is indistinguishable from magic when you first experience it. I was blown away when I first experienced this and it still feels incredible when the lines of code fly past your eyes when you are watching the LLM writing hundreds of lines of code. This is the wave that also Lovable is riding and based on their revenue numbers, they have caught lightning in a bottle.

When Lovable got founded in 2023 by two Swedes, Anton Osika and Fabian Hedin, it was not yet clear what industries AI would transform first. They were the first team to build a simple solution for anyone to build web apps by just telling the machine what you want, when most other AI programming tools focused on making technical developers more productive or lower the bar to become a developer. Osika and Hedin correctly saw that even though GPT 3.5 was not good enough for generating complex code yet, it would improve fast and if Lovable would build its service on top of it, Lovable’s product would improve with it. They would directly benefit from all the tens and hundreds of millions that would go into training new and better foundation models. I remember well my discussions with experienced developers in 2023 and none of the ones I talked to would believe that AI could one day do their work. Lo and behold, here we are in 2026 and it seems that the first thing AI is really good at is writing software because the results are verifiable unlike many other areas of work where the results are open-ended and harder for a machine to verify. That early insight when it was not yet obvious combined with the founders’ persistence until the models improved far enough for vibe coding to take off was the secret that made the early Lovable. Osika has mentioned their early vision to unlock a Cambrian explosion of people building out their ideas by enabling anyone to build software. It seems their vision is becoming closer to reality by day.

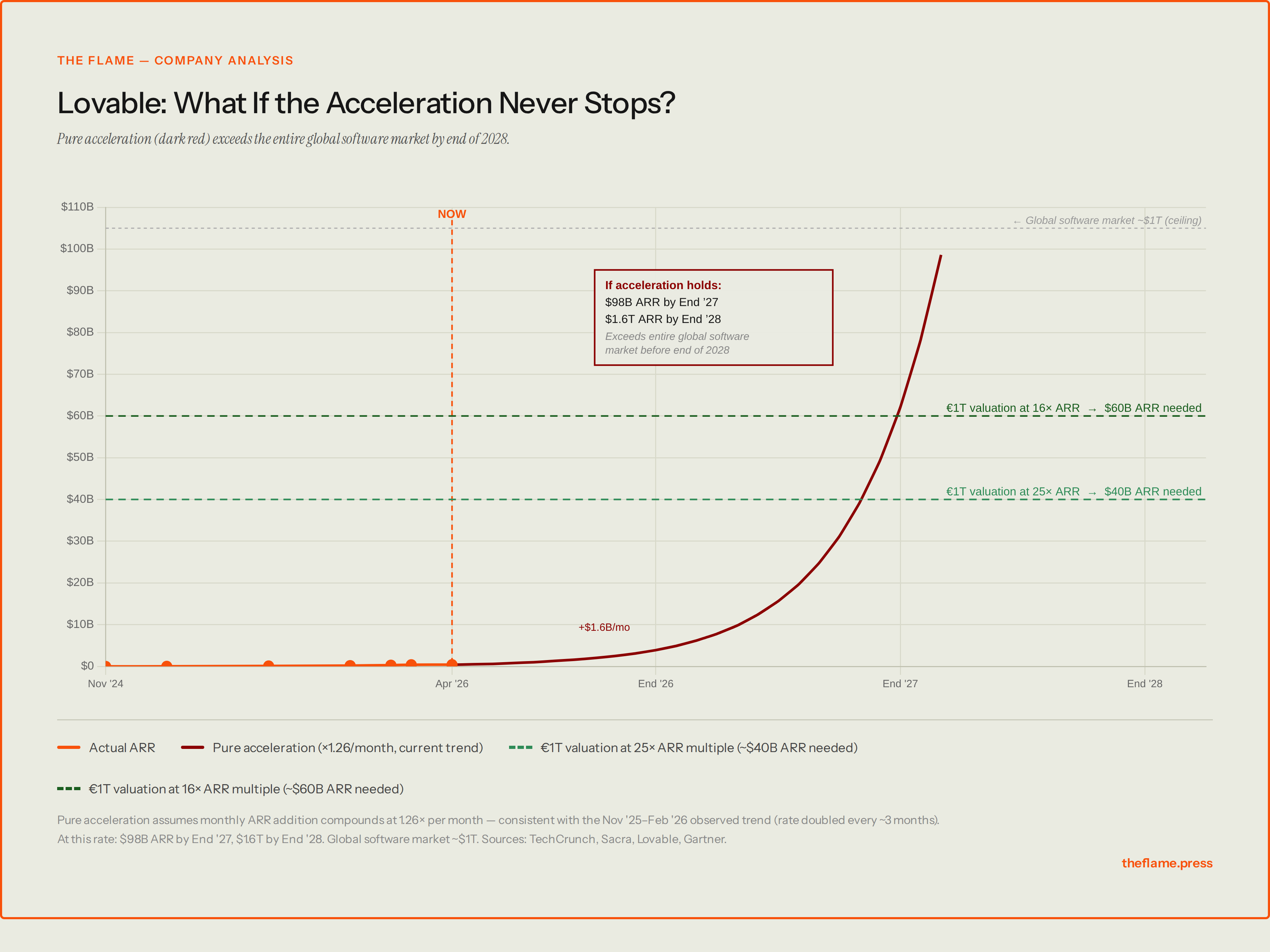

Currently Lovable’s growth is hyperbolic. It added 100M€ just this past February. The dark red line below shows what happens if the current acceleration never stops. Each successive $100M of revenue has taken half the time of the previous one: Eight months to reach $100M ARR1, four months to reach $200M ARR, two months to reach $300M ARR, one month to reach $400M ARR. The curve is not just steep but getting steeper. If we extrapolate from the growth curve, Lovable would hit $98 billion by the end of 2027 and $1.6 trillion by the end of 2028. This would make it larger than the entire software market assuming the market won’t significantly expand during that time, which it likely will if the Jevons Paradox holds true for software generation. The Jevons paradox occurs when technological advancements increase resource efficiency, making the resource cheaper and leading to higher total consumption rather than lower. Currently the price of building software is rapidly declining toward zero.

If extrapolated from early revenue growth, a lot of familiar tech companies would have looked like they hit Trillion euro valuation. At IPO in September 2020 Snowflake had roughly $530M ARR, was growing at 120% year-on-year, and listed at a $70B valuation. If we had extrapolated the Snowflake growth curve in late 2020, a trillion-dollar company was a reasonable-sounding outcome within a decade. But the growth decelerated from 120% to roughly 30% over three years. Snowflake is now worth around $50-60B — an impressive company but not a Trillion dollar story.

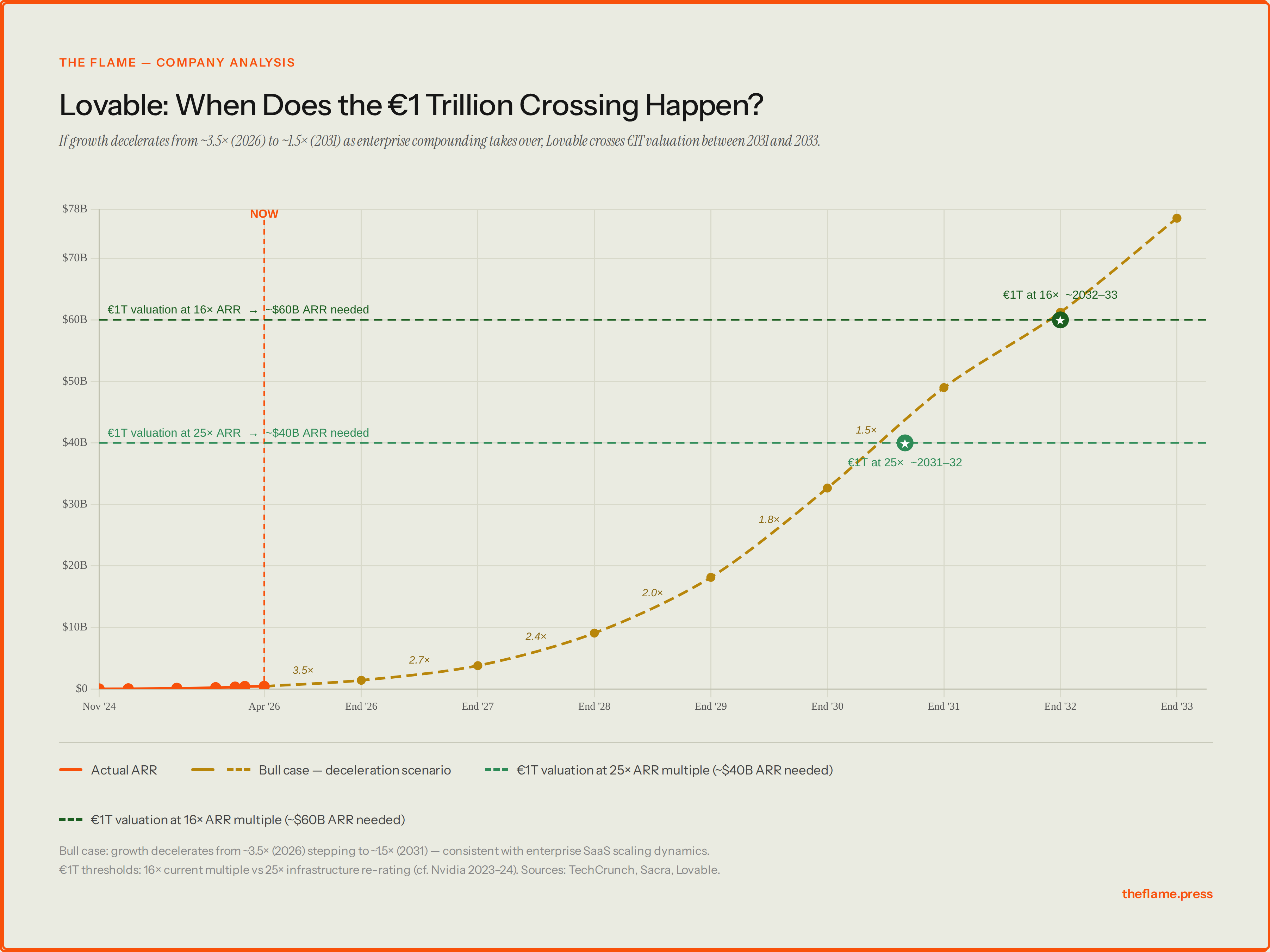

I believe Lovable is different. If Lovable decelerates as it might as the base gets larger, competition gets fiercer and enterprise becomes a larger focus, we could still see Lovable hit a Trillion euro valuation within a decade. Let me explain what I think it might look like if everything goes really right for Lovable.

The chart models a deceleration: 3.5× in 2026 as the enterprise wave hits, stepping down to 1.5× by 2031 as the base becomes larger.

The enterprise

There are a number of dangers lurking around the corner that one can point why Lovable might not get to the Trillion-euro scale, but before we look at the dangers, let’s discuss why they could get there if things go really right. That’s the business a startup like Lovable is in after all.

Traditionally consumers have been bad at paying for productivity tools. Now, there’s always the chance that AI is different and we see large numbers of consumers paying for creating their own software, but we’re not there yet for most of the market, if ever.

Putting this aside, what we do already know is that businesses are happy to pay for productivity and AI is clearly bringing that into the enterprise. Anthropic’s revenue ramp is the fastest in enterprise software history, and arguably in business history. Anthropic was at roughly $1 billion ARR in December 2024 and surpassed $30 billion in ARR in April 2026. Claude Code, Anthropic’s coding tool for developers, generated 18% of the total revenue in this February, according to Saastr, and it’s growing faster than the overall business. This enterprise demand is also where Lovable is increasingly looking at based on their product updates while at the same time holding onto its consumer offering. In fact, after Anthropic’s latest revenue numbers, this is where most of the larger players are looking at including OpenAI which this week declared enterprise its primary strategic focus for 2026, launching OpenAI Frontier, a platform for enterprises to build and manage AI agents.

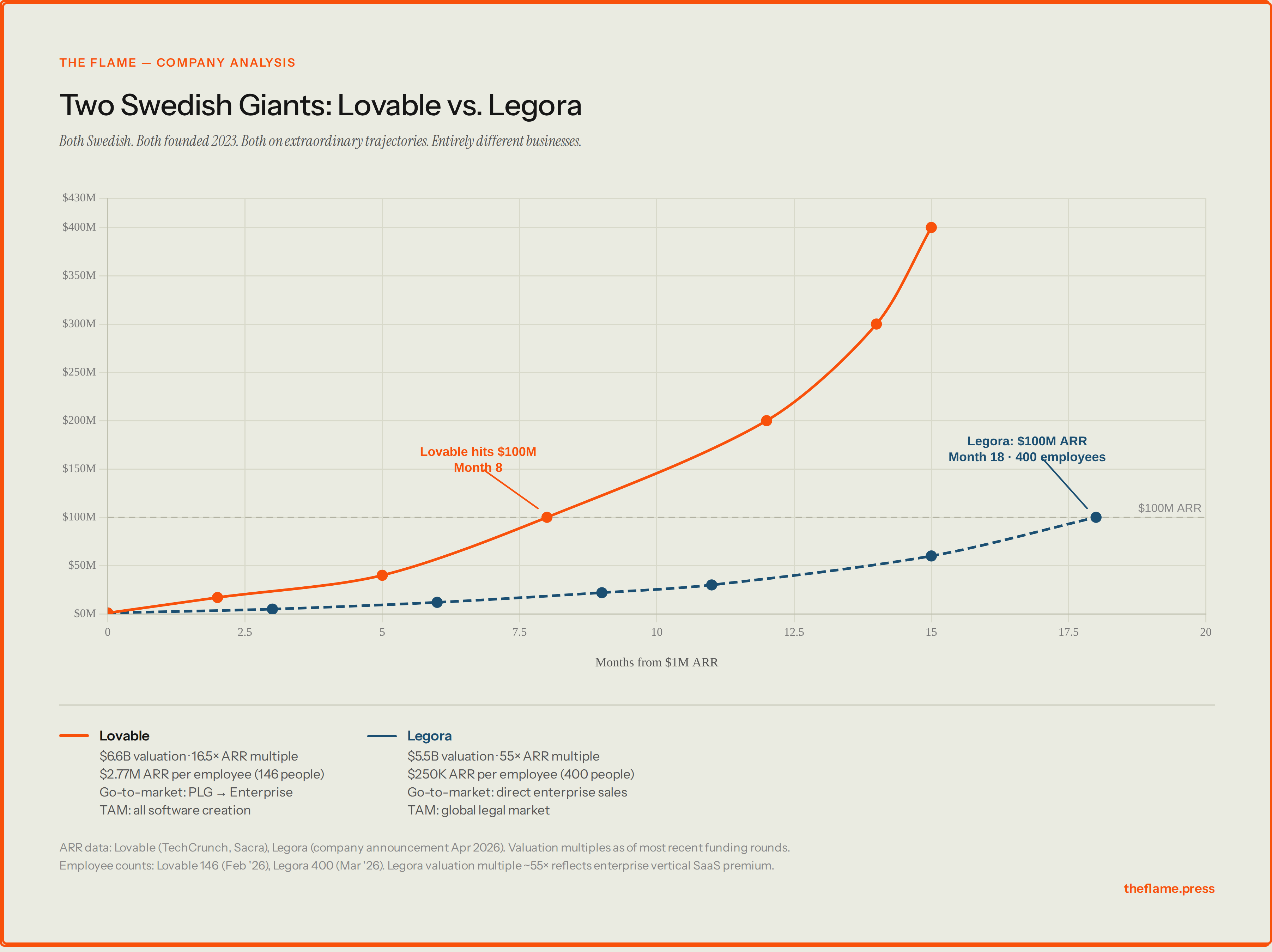

Lovable is currently trading at 16.5x multiple while its Swedish peer Legora is trading at 55x despite its much lower revenue base. This is mostly because Legora’s service is deeply embedded in the law firm workflow. The law firms it serves are willing to pay and are unlikely to churn easily. The deep integration that needs a lot heavier GTM motion compared to Lovable’s viral growth is a moat against not just Legora’s competitors like Harvey but also the large AI labs like Anthropic that both Legora and Lovable are built on top of. Even if Anthropic or OpenAI would like to vertically integrate and start servicing law firms, it’s not as straightforward as a single product update.

Such deep integration does not come automatically. Lovable generates $2.77M ARR per employee with 146 people. Legora has grown to 400 employees on $100M ARR which translates to $250K per head. Lovable is 11× more capital efficient per person. That’s the product-led-growth (PLG) model vs. direct enterprise sales trade off in action. Lovable is clearly taking enterprise seriously. The product has SOC 2 Type II and ISO 27001 certification, SSO/SAML, SCIM provisioning, role-based access control, and audit logs. This is the compliance stack enterprises require before signing contracts. The enterprise push is structurally early, but at Web Summit in November, Osika said that already more than half of Fortune 500 companies are using Lovable.

This is the bottom up go-to-market strategy that also Slack and Figma used, so they would not lose as much of the viral momentum. Osika confirmed in the 20VC podcast already in August 2025 that they are building an enterprise sales team although he also said they won’t become an enterprise company but want to focus on future founders at inception when they are starting their AI native businesses that run on software. Even so, that likely means the revenue growth acceleration slows as enterprise becomes a larger part of the revenue base, but at the same time they get deeper into the enterprise workflow which would make the product more sticky and increase Lovable’s revenue multiple. So while the revenue growth decelerates the valuation multiple goes up as they integrate deeper into the enterprise workflows.

The enterprise integration needs engineering work as we see in the different headcounts between Legora and Lovable. That’s why we’re increasingly seeing new partnerships that help with the enterprise go-to-market. Most recently Lovable has partnered with KPMG’s advisory and transformation to accelerate AI adoption among businesses whereas Replit, a US based Lovable competitor announced almost at the same time a partnership with Accenture to do the same. OpenAI announced already in February a “Frontier Alliance,” a program built around its new Frontier platform and anchored by BCG, McKinsey, Accenture and Capgemini.

The application layer

During the past 10 years SaaS was the most popular playbook for creating a valuable software company. Now we’re entering a new territory. AI applications built on top of LLMs from the large AI labs are achieving faster revenue growth than on the previous wave of SaaS applications. It’s clear that the existing SaaS winners are in danger from the faster growing AI applications, but the big question is whether the whole application layer is unstable territory to build a business on top of. We have seen how the large AI labs led by Anthropic and OpenAI can wreak havoc with a single product update. Cyber security is a good recent example of how Anthropic alone wiped off $15 billion in cyber security companies market cap by launching Claude Code Security this February, an advanced module that uses Opus 4.6 to reason through source code like a human security researcher. Just last week Anthropic released Mythos, a model so capable at finding and exploiting software vulnerabilities that Anthropic refused to release it publicly, restricting access instead to a small group of AWS, Apple, Microsoft and Google through a new initiative called Project Glasswing. An entire category of cyber security startups faces potential obsolescence from a single model too dangerous to ship.

The most obvious place for the large AI labs to vertically integrate has been code generation because that’s the AI’s first killer application. OpenAI launched Codex and Anthropic launched Claude Code as standalone products, competing directly with startups like Cursor that are built on top of their APIs. The answer from companies like Cursor who have been able to get to a large enough scale has been to start developing their own models based on data they collect of how developers are using their products and hence rival the AI labs in these verticals by building a vertical solution but from customer relationships down vs. AI labs building it from LLMs up towards the application layer. As I mentioned above, there are screenshots circulating suggesting Anthropic is rumored to release a direct Lovable competitor which is not a dissimilar threat as Anthropic is for Cursor in their market.

When AI labs vertically integrate, the application layer companies are in clear disadvantage due to the margin pressure — AI labs can offer the same service at COGS without adding the margin so the applications built on top of their API would have to offer their products at a loss to be able to compete. In addition, new applications have to pay for the customer acquisition whereas the leading AI labs already have a huge horizontal customer base so they can just choose where to vertically integrate. This is why the most well positioned AI applications are B2B products that are in industries that need deep integration and require understanding unique customer specific workflows and have data feedback loops like Legora which we discussed above.

The big question is how deep Anthropic and OpenAI will ultimately vertically integrate and whether we can build large enduring end-to-end enterprise grade products on top of Anthropic or OpenAI APIs. The uncertainty can already be seen in the revenue multiples or public SaaS P/E ratios. This is also the question determining how much Lovable can add value when it’s built on top of Anthropic API. Currently Lovable adds value by offering a fully integrated product experience out of the box for non-technical users compared to Claude which mostly targets developers when it comes to building software.

When you build an app with Lovable it has its own persistent URL, a database, a state, users can login, payments work. When you ask Claude to build something it only exists in the Claude app and does not run in the real world without further work. The other differentiation is the enterprise features I mentioned above that Lovable is now building that includes workspace knowledge, team collaboration, SOC 2 compliance, SCIM provisioning, etc.

The market has shown how much money there is to be made, so it’s likely that all the larger players including AI labs like Anthropic and OpenAI, application layer companies like Lovable and Replit as well as hyper scalers like Microsoft Copilot and Google Gemini will eventually converge on enterprise market. How Lovable will succeed has less to do with where they started, but how they play their cards now that they are at large enough scale and have the resources to train their own models if they wish.

Lovable needs to learn to build infrastructure to expand their offering beyond their individual products while the larger AI labs are learning to build products on top of their existing infrastructure. Cursor example is showing that training a narrow vertical model of your own with proprietary user data is not prohibitively expensive especially if you leverage the open source models. Lovable is already using a load balancer between different model providers that ensures consistent performance despite provider outages, rate-limiting, slow responses, and streaming responses that fail mid-generation. The load balancer is also a data moat. Every token routed through Lovable's system is a training signal for a vertical-specific code generation model. With more than a billion tokens per minute flowing through a specific and narrow stack — React, TypeScript, Tailwind, Supabase — Lovable is accumulating exactly the kind of uniform, high-quality dataset that Cursor used to build a proprietary model for developer completions. The foundation model dependency that looks like a structural weakness today becomes less acute as the dataset compounds.

Unprecedented market expansion

When the underlying capabilities improve and when Lovable keeps offering tightly integrated products that cover ever more enterprise needs, it’s not unrealistic to see how even the non-technical users could replace many of the relatively costly SaaS products they currently use in the enterprise by building new custom software using Lovable to help them in their daily work. This would swallow the two ways how enterprises consume software: Custom software that companies currently build for their needs which require developers, time and money, as well as the packaged software industry composed of products like Salesforce, Notion, Workday and Zendesk. If the cost of building custom software approaches zero the entire logic of packaged software breaks down, and if anyone can build these software products you don’t just not need the armies of developers anymore but the amount of software explodes when there are so many more people creating it.

Combined with the consumer facing product, this starts to look like a platform for creating all the software we need in- and outside of enterprise, all ready to go by using just Lovable. If we take a cue from Lovable’s slogan “Building the last piece of software”, this is the massive opportunity the company is building towards.

Lovable has already proven the massive consumer demand for their product. The enterprise SaaS market size is an additional $500B, but when we unlock all the non-technical workers’ ability to create software the market could become one of the largest markets in the world of any product ever. This potential market expansion includes all the non-technical workers in large enterprises that have not been able to build software products before as well as millions of small and medium sized businesses that SaaS companies have overlooked due to high user acquisition cost relative to the potential revenue. This is before counting all the future founders Osika has said Lovable is building for. Lovable is not only capturing the existing market, but expanding it into the largest market we have ever seen.

Momentum is a moat

Writing about Lovable’s future potential reminds me of Peter Thiel’s comment about the mistake he made with Facebook’s B round financing. Thiel assumed that going from 100 Billion to 1 Trillion must be harder than going from 1 Billion to 10 Billion but he concluded that it’s actually the easiest step. The larger you are and the faster you are moving, the more likely it is you will get even larger. Put another way, whenever companies have an unprecedented momentum, people underestimate it, and not just investors but also people inside the company.

Peter Thiel on returns to scale and why counterintuitively, the bigger you are the easier it is to get bigger as a technology company.

The tell of Lovable’s potential is not just its own revenue growth, but how fast Anthropic hit a 30B ARR. Anthropic grew from $14B to $30B in roughly eight weeks. That is still mostly tokens used by developers. Lovable is planning to take this to the rest of us. We have never seen a market that big. This is turning out to be the largest prize in the history of software, and everyone with momentum is converging on it. OpenAI turning toward the enterprise, Anthropic eyeing the application layer, Replit partnering with Accenture. Lovable has its unique starting point to take the market and it’s going after it with its chosen go-to-market strategy. Today the big headlines are about the size of the current enterprise market but when the cost of generating software approaches zero, how we build and run companies might look very different, and as Osika has said, these future founders are the ones Lovable is building for. In this new world everyone will be able to build software, and the companies that become the gateways to that will be incredibly valuable.

My argument is not that Lovable is a guaranteed winner or that it will hit a Trillion euro valuation, but that it has a real shot at becoming one and that’s rare. It’s growing its revenue from a larger base at a pace that no other European company can rival and which could take it to a Trillion euro valuation in under a decade. Osika’s decision to build GPT Engineer, an open source library for code gen that predated Lovable’s founding, gave him a window into the future before it was obvious to others: Software would be built differently in the future and anyone should be able to do it. This was the secret that Lovable was founded on. Acting on it and founding Lovable gave the founders a real shot at building the first Trillion euro company. Whether they get there is up to what they do next, and I for one am rooting for them.

Lovable determines ARR by taking the prior month’s revenue, multiplying it by 12, and annualizing the result.